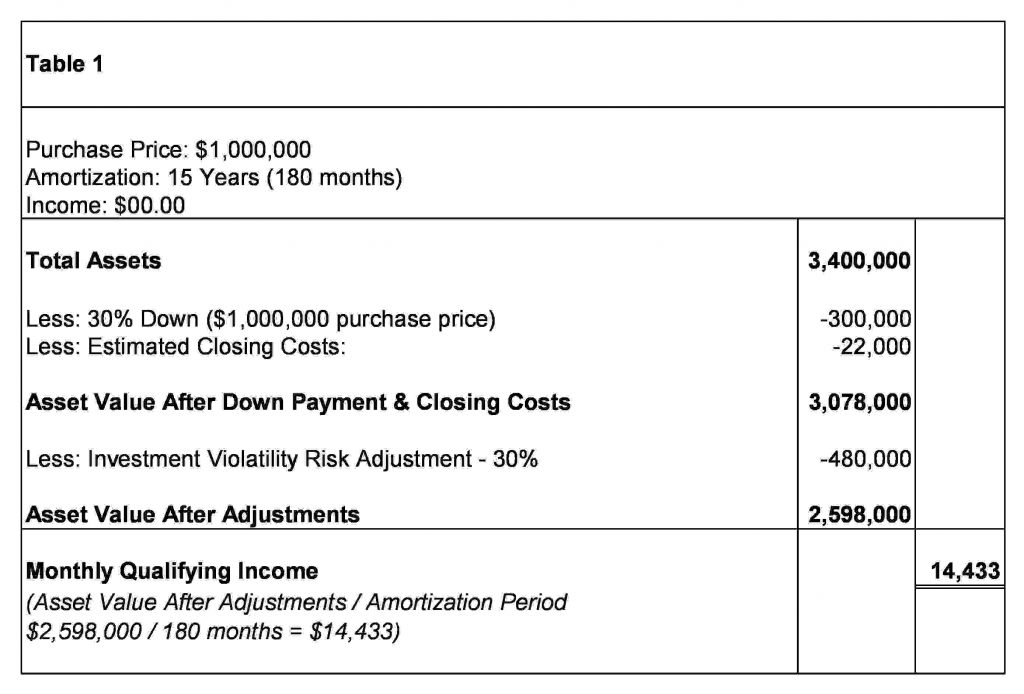

When we discuss Asset Depletion, invariably a number of questions arise. As such, let’s note a few things at the outset: 1) This product can be used if you have zero ($0) income, OR to supplement other income appearing on your mortgage application; 2) In accordance with the terms of the loan, a borrower’s assets are not consumed or depleted. Asset Depletion is a financial figment used for qualifying purposes (i.e., the lender assumes that the borrower could deplete their assets over a period of time to make the payments); 3) You are not required to disclose ALL assets you own, just those you want considered for qualifying purposes; and, 4) Assets are not required to be sold, pledged or encumbered in any way (all of your dollars continue to work 24/7 – without restriction).

With that said, let’s get started. Asset depletion is an underwriting technique in which your lender calculates the value of your assets, and makes adjustments to account for down payment, closing costs, and the inherent volatility of your investment portfolio. To establish your monthly qualifying income, the adjusted value of your assets is then divided by the number of months in the life of the proposed loan.

For example, let’s assume you’re currently unemployed, but you’ve got a total of $3,400,000 in assets allocated among the following types of accounts: