If You Want To Lower Your Mortgage Payments

You’ve Come To The RIght Place.

Here are a few of our reduced payment options. We’re sure

something here offers the payment relief you’re seeking.

INTEREST ONLY LOANS

The typical mortgage is fully amortized which means that each month’s payment consist of principal and interest. Each time a payment is made the principal balanced is reduced. Since interest accrues on the unpaid principal balance the interest paid the following month is also reduced. On an interest-only loan the borrower opts to pay the interest only with nothing applied to the principal each month.

For example, on a $400,000 mortgage, fixed for 30 years, with a 3.5% interest rate, the monthly principal and interest payment is $1,796.18. The interest-only payment would be $1,166.67. As such, the interest- only monthly payment is $629.51 less.

The interest-only option isn’t for everyone, but if you need immediate payment relief for a season, perhaps 2 – 5 years, it’s a good option. Even if you opt for a 5 year interest-only loan that converts to full amortization at the beginning of year 6, you always have the option to make the fully amortized payment sooner if you’re financially ready.

40 YEAR LOANS

In our previous example we assumed a $400,000 mortgage, fixed for 30 years, with a 3.5% interest rate, and a fully-amortized (principal & interest) payment of $1,796.18.

If we amortize the same loan for 40 years instead of 30 years, the fully-amortized payment would be $1,549.56, or $246.62 less each month.

In this instance, the 40 year loan saves you about 14% on mortgage payments. If the need for payment relief is more important than paying off the loan faster, or for some reason you don’t anticipate ever paying off the loan, the 40 year term may work for you.

DEBT CONSOLIDATION LOANS

Debt consolidation loans are among our most popular products, and for good reason. They allow our clients to maximize their equity capital by consolidating high interest credit cards, car loans, student loans, and other higher rate debt into their mortgage at today’s low mortgage rates.

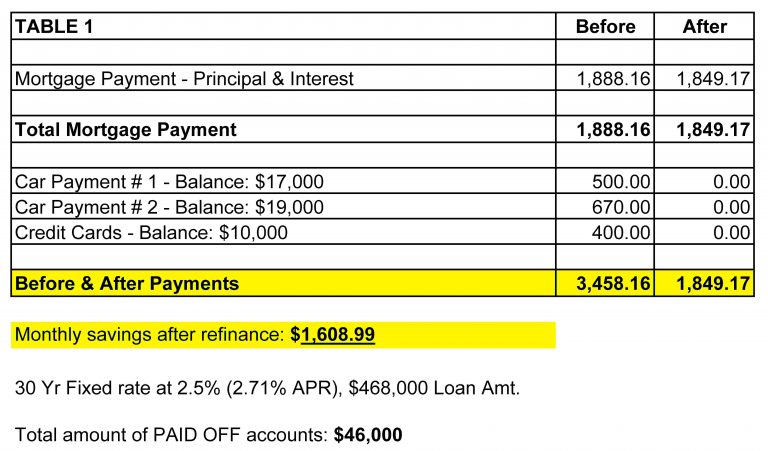

For example, we had a client who came to us with a $1,888.16 mortgage payment, and a 4.5% rate, fixed for 30 years. In addition, they had two car payments totaling $1,170, and $400 per month in credit card payments. We refinanced their mortgage into a new 2.50% (2.71% APR)

fixed rate, paid off both cars and all the credit cards, saving the client $1,608.99 per month.

In addition, the client was able to skip two (2) payments. If you need quick payment relief, this is the way to go.

See Table 1 below for a before and after compariso

INTEREST RATE BUYDOWN

There are two types of interest rate buydowns in the mortgage industry, permanent and temporary.

Permanent Buydown: A permanent rate buydown permits a borrower to lower the interest rate on their mortgage by paying a percentage of the loan amount in advance to obtain the lower rate. For example, assume you’re borrowing $400,000 and you’ve been quoted a rate of 4.5% on a 30 year fixed rate mortgage. At that rate your monthly principal and interest payment would be $2,026.74 and the amount of interest you’d pay over the life of the loan is $329,626.85. If you paid a lump sum up front, you could buy the rate down to let’s say 3.875%. At 3.875% your monthly payment would be $1,880.95, and the interest you’d pay over the life of the loan would be $277,141.40. As you can see, a rate buydown would save you $145.79 per month, and $52,485.45 in interest over the life of the loan.

Temporary Buydown: Temporary rate buydowns are also available, but they’re structured a little differently in work a little differently. This time let’s assume you’re buying a home, and seeking a mortgage of $400,000. You’ve been quoted a rate of 5.5% on a 30 year fixed rate mortgage. At that rate your monthly principle and interest payment would be $2,271.16. That payment is really at the outer limits of your comfort zone, and if possible you’d like it reduced, particularly in the first 2 – 3 years.

There is a rate reduction technique called a 3-2-1 buydown that reduces your interest rate by 3% your first year in the loan, by 2% your second year, and by 1 % your third year. So with a quoted rate of 5.5%, here’s how the numbers would work out on a 3-2-1 buydown:

Year 1: Payment of $1,580.48 at an interest rate of 2.5%

Year 2: Payment of $1,796.18 at an interest rate of 3.5%

Year 3: Payment of $2,026.74 at an interest rate of 4.5%

Years 4 – 30: Payment of $2,271.16 at an interest rate of 5.5%

As illustrated above, the payments in years 1, 2 & 3 are based on temporarily reduced (bought down) rates, allowing you to “ease” into the permanent payment of $2,271.16 from years 4 – 30.

The amount needed to effect a 3-2-1 buydown can be negotiated with your lender, and depends on the loan type, interest rate, loan-to-value, and other factors. The 3-2-1 buydown can be a significant tool for new homeowners as they get used to having a mortgage payment.

GRADUATED MORTGAGES

A Graduated Mortgage is a fixed rate mortgage that’s amortized with lower payments in the earlier years, and gradually increases payments as the years progress. The lower initial payments, and interest rate, is to help more people qualify to purchase a home.

The idea is that the borrowers income will increase over time. So the loan is partially based on anticipated upward mobility of the borrower. If you anticipate that your income will gradually increase over time this option could be a great choice. If you don’t have a realistic expectation that that your income will rise over time, a graduated payment mortgage could be a source of stress as the monthly payment increases.

Let’s assume you’re obtaining a $300,000, 30 year fixed rate mortgage, with a 3% interest rate. The monthly principal & interest payment would be $1,264.81.

The typical Graduated Mortgage would require 5 increases, of 5% each, over a 5 year period; or, 10 increases, of 2% each, over a 10 year period. Here’s how it breaks down over time:

Scenario 1: 5, 5% Adjustments, In 5 Years

Initial Payment: $1,264.81

1st Year 5% Payment Adjustment: $1,328.05

2nd Year 5% Payment Adjustment: $1,394.45

3rd Year 5% Payment Adjustment: $1,464.18

4th Year 5% Payment Adjustment: $1,537.38

5th Year 5% Payment Adjustment: $1,614.25

Scenario 2: 10. 2% Adjustments, In 10 Years

Initial Payment: $1,264.81

1st Year 2% Payment Adjustment: $1,290.11

2nd Year 2% Payment Adjustment: $1,315.91

3rd Year 2% Payment Adjustment: $1,342.23

4th Year 2% Payment Adjustment: $1,369.07

5th Year 2% Payment Adjustment: $1,396.45

6th Year 2% Payment Adjustment: $1,424.83

7th Year 2% Payment Adjustment: $1,452.87

8th Year 2% Payment Adjustment: $1,481.93

9th Year 2% Payment Adjustment: $1,511.56

10th Year 2% Payment Adjustment: $1,541.80

As evidenced by the sample payment schedules above, Graduated payments are not overwhelming, and when matched with an upwardly mobile borrower, can produce a result that creates new homeowners who may have otherwise not qualified.

REVERSE MORTGAGES

Reverse mortgages require no monthly payments and are designed for homeowners 62 years of age or older. This product caters to the need of seasoned homeowners who may be faced with economic difficulties stemming from reduced or fixed income, along with increased health or subsistence costs. Reverse mortgages allows us to grow older with dignity, freedom, and peace of mind knowing we have the option to stay in our homes. On the other hand, there may not be any difficulties at all. You may just want some extra cash to travel, open a business, produce a small local play, or otherwise complete your bucket list. There is no restriction on what you can do with your money.

It’s called a reverse mortgage because it’s just the opposite of a traditional mortgage. Instead of making payments to the lender, the lender makes payments to you. Payments to you are made out of the equity in your home, in accordance with the payment option you choose.

There are a number of ways you can receive payments:

- If you obtain a fixed rate reverse mortgage, you can receive a lump sum cash single disbursement.

If you obtain an adjustable rate reverse mortgage, you’ll have a number of options for receiving your payments:

- You can receive equal monthly payments for a fixed period of time.

- You may receive equal monthly payments for as long as you live in your home.

- A line of credit can be established allowing you to draw cash as needed (you’ll only pay interest on the funds you access).

- Another option is to receive both fixed payments for life and a line of credit.

- Combine equal monthly payments for a fixed period of time, with a line of credit.

In addition to receiving cash, a reverse mortgage may also be used to purchase a principal residence, or to refinance an existing reverse mortgage

A reverse mortgage is not required to be repaid unless or until:

- the borrower dies;

- the borrower moves permanently from the home;

- the borrower transfers title to the home; or

- the borrower fails to meet their obligations under the mortgage, as set in the mortgage terms.

Upon receiving a reverse mortgage you’re still responsible for certain obligations:

- property taxes;

- hazard insurance;

- flood insurance, if applicable;

- ground rents, if applicable;

- condominium fees, if applicable;

- planned unit development fee, if applicable;

- homeowners’ association fees, if applicable; and

- any other special assessments levied by state or federal governments.

Reverse mortgages can be an awesome option for eliminating mortgage payments, but aren’t perfect for everyone. Additional terms and restrictions apply.

(Please note that the information above applies to the U.S. government insured reverse mortgage program because it provides more protections for our clients. The information does not encompass available private programs).

To find out more about Reduced Payment Mortgages, please contact us today.

Call 855.SLG.FUND (855.754.3863) or inquire below.

Square Peg? Round Hole?

We can help you.